Buried in the Toronto Economic Bulletin (warning: Excel document) is a column listing the number of passengers passing through Pearson International Airport (YYZ) each month, going back more than fifteen years. There’s a story to tell in the forecast, too:

Flight data are a great forecasting example because they display such clear

seasonal patterns, in this case peaking in the summer months and falling off in

the winter. R has excellent tools for working with time series data and whipping

up simple forecasts like this one. But there’s some friction with the modern

tidyverse tools, because the latter expect a data.frame as the common

interchange format.

In this post, I’ll outline an approach to fitting many time series models using the tidyverse tools, including model selection for out-of-sample performance. To ease the transition between these two worlds I make extensive use of list columns and the broom package.

The Set Up

For this post I’ve extracted the data into a vector of R’s built-in ts class,

which is the common interchange format for most time series packages. As of

writing, I have data from January 2000 through August 2016.

# load("path/to/passengers.rda")

str(passengers)

## Time-Series [1:200] from 2000 to 2017: 2072798 2118150 2384907 2260620 2386165 2635018 2788843 2942082 2477000 2527969 ...

You’ll also need the following packages, all of which are staples of the tidyverse except for forecast, which is a prominent time series forecasting package for R:

suppressMessages({

library(dplyr)

library(tidyr)

library(purrr)

library(broom)

library(ggplot2)

library(forecast)

})

Time Series Forecasting in R

There are an overwhelming number of time series models used for forecasting out there (see the CRAN task view on time series for a sense of what’s available in R alone), but the most common ones are probably ARIMA and ETS, both of which can handle seasonal data sets like this one.

In choosing a model for forecasting, what we care about is the accuracy of the model on unseen (that is, out-of-sample) data. Since we don’t have a way of measuring that directly, we simulate the experience by holding out a test set.

The nature of the autocorrelated errors in time series data mean that randomly selecting training and test sets (or, indeed, using traditional bootstrap or cross-validation) will erase much of the information in the data, so common practice with time series data is to hold out the last few observations, ideally the same interval as you’d like to forecast over.1

I’ll mention that this risks overfitting to this particular test set, something I’ll return to below. (As the statistician Andrew Gelman has remarked, it is important to realise that test sets and cross validation are estimates of out-of-sample performance, not a direct measure.)

For this post I’m going to hold out the two most recent years' worth of data as

a test set. R provides a convenient window function for breaking up time

series:

train <- window(passengers, end = c(2014, 8))

test <- window(passengers, start = c(2014, 9))

We can use this training set to fit some ARIMA and ETS models, and see how they compare.

Fitting ARIMA Models in R

R has built in support for fitting ARIMA models with, you guessed it, the

arima() function. However, there are a number of shortcomings to this

implementation, so I’d recommend using the Arima() version from the

forecast package instead. You can also try your luck with the package’s

auto.arima() function, which will try and find an optimal model automatically.

Choosing the order of an ARIMA model usually benefits from some manual

exploration of the autocorrelated errors, especially using the

forecast::tsdisplay() plot. For brevity I won’t walk you through the process

here, but I’d strongly recommend taking a look at Rob Hyndman and George

Athanasopoulos' chapter on forecasting seasonal data using ARIMA,

which is freely available online.

For now, auto.arima() should do just fine. It’s worth experimenting with the

approximations disabled, as follows:

arima.fit <- forecast::auto.arima(train, d = 1, D = 1,

stepwise = FALSE,

approximation = FALSE)

arima.fit

## Series: train

## ARIMA(0,1,1)(0,1,1)[12]

##

## Coefficients:

## ma1 sma1

## -0.1927 -0.6731

## s.e. 0.0774 0.0675

##

## sigma^2 estimated as 6.925e+09: log likelihood=-2080.57

## AIC=4167.15 AICc=4167.3 BIC=4176.43

The automatic process selects an ARIMA model with low order, indicating that a simple model might fit this data reasonably well.

Fitting ETS Models in R

The forecast package also provides an ets function, which by default will

choose an optimal model:

ets.fit <- forecast::ets(train, model = "ZZZ")

ets.fit

## ETS(A,N,A)

##

## Call:

## forecast::ets(y = train, model = "ZZZ")

##

## Smoothing parameters:

## alpha = 0.7467

## gamma = 1e-04

##

## Initial states:

## l = 2373863.6415

## s=-155048.7 -371915.5 -66744.27 -9469.378 562836.6 411528.9

## 104613.3 -2894.734 -101326.8 65840.67 -269851.6 -167568.5

##

## sigma: 79047.8

##

## AIC AICc BIC

## 4909.794 4912.794 4957.351

Notice that this (ostensibly optimal) model has an AICc of 4912.794, which is much higher than the ARIMA models explored above. This may be an indication that ETS models are not a good fit for this data set.

Fitting Many Models using List-Columns and Purrr

One can choose both an ARIMA and ETS model based on how well it fits the training data. However, when forecasting, better out-of-sample performance is the true goal. For this reason, I’m going to take a more systematic approach, fitting a wide variety of both ETS and ARIMA models and comparing their out-of-sample performance.

Inspired by the general coherence of the tidyverse, I believe all of this can be organized into a tidy data frame, with one model per row. I use the following approach:

- Create columns for training data, modelling functions, and any other model parameters.

- Wrap these training data and model parameters into a single

paramcolumn. - Use

purrr::invoke_map()to apply the modelling function to these model parameters; and - Use

purrr::map()and friends (orbroom::glance()) to extract goodness of fit measures.

To start with, we create data sets of models and their parameters. The following

will generate a data frame of all possible ETS models (check out ?ets for

details):

ets.params <- tidyr::crossing(

error = c("A", "M"), trend = c("N", "A", "M"),

seasonal = c("N", "A", "M"), damped = c(TRUE, FALSE)

) %>%

# Drop combinations with a damped non-trend.

mutate(drop = ifelse(trend == "N" & damped, TRUE, FALSE)) %>%

filter(!drop) %>%

# Create labels for the models out of these parameters.

mutate(kind = "ETS",

desc = paste0("(", error, ",", trend,

ifelse(damped, "d", ""),

",", seasonal, ")"),

model = paste0(error, trend, seasonal)) %>%

# Drop nonsensical models (these are flagged by `ets` anyway).

filter(!model %in% c("MMA", "AMN", "AMA", "AMM",

"ANM", "AAM")) %>%

select(kind, desc, model, damped)

ets.params

## # A tibble: 19 × 4

## kind desc model damped

## <chr> <chr> <chr> <lgl>

## 1 ETS (A,A,A) AAA FALSE

## 2 ETS (A,Ad,A) AAA TRUE

## 3 ETS (A,A,N) AAN FALSE

## 4 ETS (A,Ad,N) AAN TRUE

## 5 ETS (A,N,A) ANA FALSE

## 6 ETS (A,N,N) ANN FALSE

## 7 ETS (M,A,A) MAA FALSE

## 8 ETS (M,Ad,A) MAA TRUE

## 9 ETS (M,A,M) MAM FALSE

## 10 ETS (M,Ad,M) MAM TRUE

## 11 ETS (M,A,N) MAN FALSE

## 12 ETS (M,Ad,N) MAN TRUE

## 13 ETS (M,M,M) MMM FALSE

## 14 ETS (M,Md,M) MMM TRUE

## 15 ETS (M,M,N) MMN FALSE

## 16 ETS (M,Md,N) MMN TRUE

## 17 ETS (M,N,A) MNA FALSE

## 18 ETS (M,N,M) MNM FALSE

## 19 ETS (M,N,N) MNN FALSE

With this set of model parameters in hand, we can create list columns containing

the training data and the function to compute the model (ets in this case). We

can also wrap up the parameters into a param list column by using the curious

but useful transpose() function.

ets.models <- ets.params %>%

# Add in the training set and the modelling function.

mutate(fn = replicate(forecast::ets, n = n()),

train = replicate(list(train), n = n())) %>%

# Create a "param" column to pass to `fn`.

mutate(params = purrr::transpose(list(

"y" = train, "model" = model, "damped" = damped

))) %>%

select(kind, desc, train, fn, params)

ets.models

## # A tibble: 19 × 5

## kind desc train fn params

## <chr> <chr> <list> <list> <list>

## 1 ETS (A,A,A) <S3: ts> <fun> <list [3]>

## 2 ETS (A,Ad,A) <S3: ts> <fun> <list [3]>

## 3 ETS (A,A,N) <S3: ts> <fun> <list [3]>

## 4 ETS (A,Ad,N) <S3: ts> <fun> <list [3]>

## 5 ETS (A,N,A) <S3: ts> <fun> <list [3]>

## 6 ETS (A,N,N) <S3: ts> <fun> <list [3]>

## 7 ETS (M,A,A) <S3: ts> <fun> <list [3]>

## 8 ETS (M,Ad,A) <S3: ts> <fun> <list [3]>

## 9 ETS (M,A,M) <S3: ts> <fun> <list [3]>

## 10 ETS (M,Ad,M) <S3: ts> <fun> <list [3]>

## 11 ETS (M,A,N) <S3: ts> <fun> <list [3]>

## 12 ETS (M,Ad,N) <S3: ts> <fun> <list [3]>

## 13 ETS (M,M,M) <S3: ts> <fun> <list [3]>

## 14 ETS (M,Md,M) <S3: ts> <fun> <list [3]>

## 15 ETS (M,M,N) <S3: ts> <fun> <list [3]>

## 16 ETS (M,Md,N) <S3: ts> <fun> <list [3]>

## 17 ETS (M,N,A) <S3: ts> <fun> <list [3]>

## 18 ETS (M,N,M) <S3: ts> <fun> <list [3]>

## 19 ETS (M,N,N) <S3: ts> <fun> <list [3]>

And now we can make use of invoke_map() to fit all of these models. I’ve also

extracted the AICc values of each for comparison.

ets.fits <- ets.models %>%

# Fit the models, and extract the AICc.

mutate(fit = purrr::invoke_map(fn, params),

aicc = purrr::map_dbl(fit, "aicc")) %>%

arrange(aicc)

ets.fits

## # A tibble: 19 × 7

## kind desc train fn params fit aicc

## <chr> <chr> <list> <list> <list> <list> <dbl>

## 1 ETS (A,N,A) <S3: ts> <fun> <list [3]> <S3: ets> 4912.794

## 2 ETS (M,N,M) <S3: ts> <fun> <list [3]> <S3: ets> 4914.492

## 3 ETS (A,A,A) <S3: ts> <fun> <list [3]> <S3: ets> 4923.181

## 4 ETS (A,Ad,A) <S3: ts> <fun> <list [3]> <S3: ets> 4925.173

## 5 ETS (M,Ad,M) <S3: ts> <fun> <list [3]> <S3: ets> 4925.813

## 6 ETS (M,Md,M) <S3: ts> <fun> <list [3]> <S3: ets> 4926.635

## 7 ETS (M,N,A) <S3: ts> <fun> <list [3]> <S3: ets> 4928.246

## 8 ETS (M,Ad,A) <S3: ts> <fun> <list [3]> <S3: ets> 4941.445

## 9 ETS (M,A,A) <S3: ts> <fun> <list [3]> <S3: ets> 4942.699

## 10 ETS (M,A,M) <S3: ts> <fun> <list [3]> <S3: ets> 4977.796

## 11 ETS (M,M,M) <S3: ts> <fun> <list [3]> <S3: ets> 4985.782

## 12 ETS (M,M,N) <S3: ts> <fun> <list [3]> <S3: ets> 5283.217

## 13 ETS (M,N,N) <S3: ts> <fun> <list [3]> <S3: ets> 5283.227

## 14 ETS (M,A,N) <S3: ts> <fun> <list [3]> <S3: ets> 5285.426

## 15 ETS (M,Ad,N) <S3: ts> <fun> <list [3]> <S3: ets> 5285.783

## 16 ETS (M,Md,N) <S3: ts> <fun> <list [3]> <S3: ets> 5286.098

## 17 ETS (A,N,N) <S3: ts> <fun> <list [3]> <S3: ets> 5301.575

## 18 ETS (A,Ad,N) <S3: ts> <fun> <list [3]> <S3: ets> 5305.353

## 19 ETS (A,A,N) <S3: ts> <fun> <list [3]> <S3: ets> 5308.133

Note that the best-performing model here — ETS(A,N,A) — is the same one

arrived at automatically above.

We can do the same thing with the ARIMA models: generate a list of model

parameters as a data frame, collect these into a param list-column, and then

fit the function using invoke_map(). Unlike ETS, there are an infinite number

of possible ARIMA models. However, we can guess from above that good models will

have low order.

arima.params <- tidyr::crossing(ar = 0:2, d = 1:2, ma = 0:2,

sar = 0:1, sma = 0:1) %>%

# Create a label for the model.

mutate(kind = "ARIMA",

desc = paste0("(", ar, ",", d, ",", ma, ")(",

sar, ",1,", sma, ")")) %>%

group_by(kind, desc) %>%

# This has to be done rowwise to avoid the flattening

# behaviour of c().

do(order = c(.$ar, .$d, .$ma),

seasonal = c(.$sar, 1, .$sma)) %>%

ungroup()

arima.models <- arima.params %>%

# Add in the training set and the modelling function.

mutate(fn = replicate(forecast::Arima, n = n()),

train = replicate(list(train), n = n())) %>%

# Create a "param" column to pass to `fn`.

mutate(params = purrr::transpose(list(

"y" = train, "order" = order, "seasonal" = seasonal

))) %>%

select(kind, desc, train, fn, params)

arima.fits <- arima.models %>%

# Fit the models, and extract the AICc.

mutate(fit = purrr::invoke_map(fn, params),

aicc = purrr::map_dbl(fit, "aicc")) %>%

arrange(aicc)

arima.fits

## # A tibble: 72 × 7

## kind desc train fn params fit aicc

## <chr> <chr> <list> <list> <list> <list> <dbl>

## 1 ARIMA (0,2,2)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4157.528

## 2 ARIMA (1,2,1)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4157.796

## 3 ARIMA (0,2,2)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4158.203

## 4 ARIMA (1,2,1)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4158.223

## 5 ARIMA (2,2,1)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4159.600

## 6 ARIMA (1,2,2)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4159.658

## 7 ARIMA (2,2,1)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4160.292

## 8 ARIMA (1,2,2)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4160.306

## 9 ARIMA (0,2,1)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4160.888

## 10 ARIMA (0,2,1)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4161.533

## # ... with 62 more rows

Since this data frame has the same form as the one used for the ETS models, we

can concatenate them into a master list of models. The forecast() function is

its namesake package’s universal forecasting function. We can use it to add a

column of the two-year forecast for all of these models.

yyz.forecasts <- dplyr::bind_rows(ets.fits, arima.fits) %>%

mutate(forecast = map(fit, forecast::forecast, h = 24)) %>%

arrange(aicc)

yyz.forecasts

## # A tibble: 91 × 8

## kind desc train fn params fit aicc

## <chr> <chr> <list> <list> <list> <list> <dbl>

## 1 ARIMA (0,2,2)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4157.528

## 2 ARIMA (1,2,1)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4157.796

## 3 ARIMA (0,2,2)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4158.203

## 4 ARIMA (1,2,1)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4158.223

## 5 ARIMA (2,2,1)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4159.600

## 6 ARIMA (1,2,2)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4159.658

## 7 ARIMA (2,2,1)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4160.292

## 8 ARIMA (1,2,2)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4160.306

## 9 ARIMA (0,2,1)(0,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4160.888

## 10 ARIMA (0,2,1)(1,1,1) <S3: ts> <fun> <list [3]> <S3: ARIMA> 4161.533

## # ... with 81 more rows, and 1 more variables: forecast <list>

Measuring Forecast Accuracy

The AICc is not a direct measure of forecast accuracy. Traditional root mean

squared error (RMSE) and mean absolute error (MAE) are both options, although

the author of the forecast package recommends mean absolute scaled error

(MASE). The package provides the accuracy() function to compute all of these

measures (and a few others) for any forecast object, but unfortunately it

returns a matrix with meaningful row names, which would be hard to wrap up

inside a list column. What we need is an API that returns a data frame.

It turns out that there is a project

devoted specifically to this problem. The broom package provides a standard

interface for “tidying” model summaries using the S3 glance() method. At the

time of writing, the package doesn’t contain an implementation for forecast

objects, but it isn’t too hard to write one using the output of

forecast::accuracy():

glance.forecast <- function(x, newdata = NULL, ...) {

res <- if (is.null(newdata)) {

acc <- forecast::accuracy(x)

tibble::as_tibble(t(acc[1,]))

} else {

acc <- forecast::accuracy(x, newdata)

tibble::as_tibble(t(acc[2,]))

}

# Format the names of the measures to suit broom::glance().

names(res) <- tolower(names(res))

if (length(names(res)) > 7) names(res)[8] <- "thielsu"

res

}

This can now be combined with tidyr::unnest() to get columns of RMSE, MAE, MASE,

and so on using map():

acc <- yyz.forecasts %>%

mutate(glance = map(forecast, broom::glance)) %>%

unnest(glance) %>%

arrange(rmse, mae, mase)

select(acc, kind, desc, rmse, mae, mase)

## # A tibble: 91 × 5

## kind desc rmse mae mase

## <chr> <chr> <dbl> <dbl> <dbl>

## 1 ARIMA (2,1,2)(1,1,1) 76061.98 51352.61 0.3289412

## 2 ETS (M,N,M) 76143.55 49990.36 0.3202153

## 3 ETS (M,Ad,M) 76387.04 50008.08 0.3203288

## 4 ETS (M,Md,M) 76595.67 50443.22 0.3231161

## 5 ETS (A,N,A) 79047.80 53876.34 0.3451071

## 6 ETS (M,N,A) 79174.58 54396.73 0.3484405

## 7 ARIMA (2,2,1)(1,1,1) 79294.88 53378.97 0.3419212

## 8 ARIMA (1,2,2)(1,1,1) 79303.39 53397.52 0.3420400

## 9 ARIMA (1,1,2)(1,1,1) 79305.25 53167.62 0.3405674

## 10 ARIMA (0,2,2)(1,1,1) 79307.55 53368.28 0.3418527

## # ... with 81 more rows

Each accuracy measure provides a slightly different ranking of models. Does this list lay out which model is best? If what you are after is forecast accuracy, the answer is no. It is overwhelmingly likely that some models which perform exceptionally well on this training data may do poorly when confronted with new data. This is precisely why we left a “test” series aside earlier.

Measuring Out-of-Sample Performance Using a Test Set

You might have noticed above that the broom::glance() implementation above

accepts a newdata parameter for out-of-sample accuracy assessment. We can

pass the test data left aside at the start of the post in the same fashion as

above, and lay out the in-sample and out-of-sample measures side by side.

This is also a great opportunity for visual exploration! I’m going to use the

ggrepel package to add cleaner labels to the top in-sample and test-set

performers, although you can also substitute the built-in

ggplot2::geom_label() here.

perf <- yyz.forecasts %>%

mutate(test = replicate(list(test), n = n()),

glance = map2(forecast, test, broom::glance)) %>%

tidyr::unnest(glance) %>%

# Pull out the out-of-sample RMSE, MAE, and MASE.

select(kind, desc, oos.rmse = rmse,

oos.mae = mae, oos.mase = mase) %>%

# Join the in-sample RMSE, MAE, and MASE columns.

inner_join(acc, by = c("kind", "desc")) %>%

rename(is.rmse = rmse, is.mae = mae, is.mase = mase) %>%

arrange(oos.rmse, is.rmse) %>%

select(kind, desc, is.rmse, oos.rmse, is.mae, oos.mae,

is.mase, oos.mase)

# Find the top four models by in-sample and out-of-sample MASE.

top.perf <- perf %>%

mutate(top.is = rank(is.mase), top.oos = rank(oos.mase)) %>%

filter(top.is <= 4 | top.oos <= 4)

library(ggrepel)

# Graph in-sample vs. out-of-sample MASE for the top 50% of each.

perf %>%

filter(oos.mase < quantile(oos.mase, 0.5) |

is.mase < quantile(is.mase, 0.5)) %>%

ggplot(aes(y = oos.mase, x = is.mase)) +

geom_point(aes(colour = kind)) +

# Vertical/horizontal lines at the minimum MASE for each sample.

geom_vline(aes(xintercept = min(is.mase)),

linetype = 5, colour = "gray50") +

geom_hline(aes(yintercept = min(oos.mase)),

linetype = 5, colour = "gray50") +

# Label the top models.

ggrepel::geom_label_repel(aes(label = paste(kind, desc)),

size = 2.5, segment.colour = "gray50",

data = top.perf) +

labs(x = "In-Sample MASE", y = "Out-of-Sample MASE",

colour = "Family")

This plot reveals some interesting patterns. First, it looks as though some of

the multiplicative ETS models do quite well on measures of in-sample accuracy,

but poorly when confronted with the test set (top left). Second, there is an

ETS (M,M,M) model that does very well on the test set, but quite unremarkably

on the training data (bottom right). To mirror this, the best in-sample

performer has only middling test set performance (middle right). Third, the

models that do well on both measures tend to be ARIMA models of low order

(bottom left).

What conclusions can we draw from this? Test set performance isn’t the ultimate

arbiter of forecasting performance. As I mentioned above, you can overfit to

this specific test set, which is probably what is going on with the high-flying

ETS (M,M,M) model. The low-order ARIMA models strike me as a better choice.

Forecasting, Finally

Okay, now that we’ve settled on a model, it’s time to actually forecast the series forward.

passengers.fc <- passengers %>%

Arima(order = c(2, 1, 2), seasonal = c(1, 1, 0)) %>%

forecast(h = 24, level = c(50, 95))

All forecast accuracy measures aside, there’s no substitute for the sense of

model performance one gets by visual inspection. The forecast object has an

implementation for the ggplot2::autoplot() S3 method in addition to the base

graphics plot(), so we can get a ggplot2 graphic very easily. The

autoplot() output doesn’t include the fitted values by default, but we can add

them manually:

autoplot(passengers.fc) +

geom_path(aes(y = as.vector(passengers.fc$fitted),

x = time(passengers.fc$fitted)),

linetype = 1, alpha = 0.5, colour = "red")

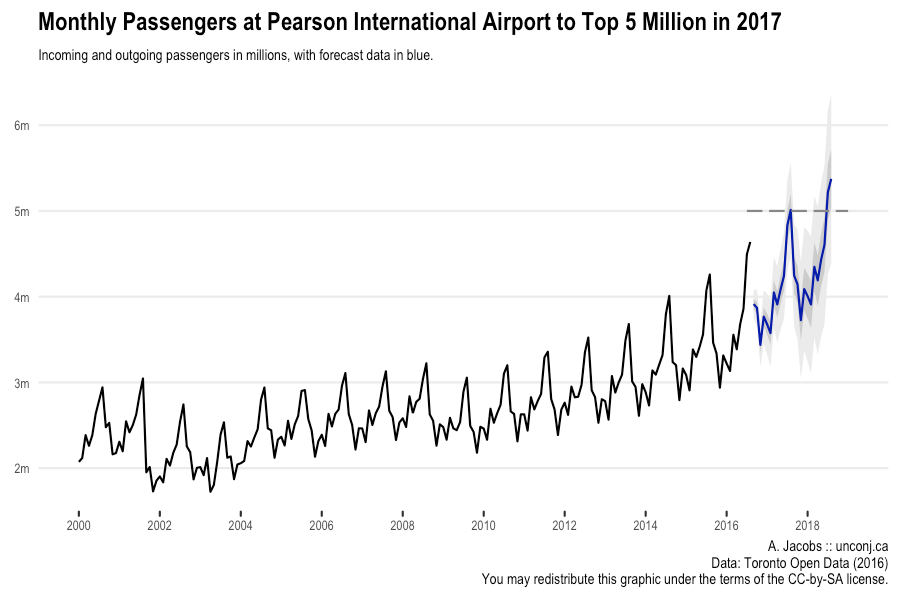

It looks like the model fits the data quite well, aside from some trouble around 2003. The forecast output also gives us a nice story to tell: monthly passengers at YYZ looks likely to break 5 million for the first time in summer 2017.

With this story in hand, you can wrap up the output of autoplot() in a pretty

theme, add some bells and whistles, and publish a nice little graphic on this

data. The code below generates the plot at the top of this post:

millions <- function(x) paste0(format(x / 1e6, digits = 2), "m")

autoplot(passengers.fc, shadecols = c("#cccccc", "#eeeeee")) +

geom_segment(aes(y = 5e6, yend = 5e6, x = 2016.5, xend = 2019),

size = 0.5, colour = "#888888", linetype = 5) +

scale_x_continuous(breaks = seq(2000, 2018, by = 2), expand = c(0, 1)) +

scale_y_continuous(labels = millions) +

theme_minimal() +

theme(legend.position = "none",

panel.grid.minor = element_blank(),

panel.grid.major.x = element_blank(),

axis.ticks.x = element_line(colour = "#333333", size = 0.5),

axis.ticks.length = grid::unit(2, units = "pt"),

text = element_text(family = "Arial Narrow", size = 8),

plot.title = element_text(size = 12, face = "bold")) +

labs(title = paste("Monthly Passengers at Pearson International Airport",

"to Top 5 Million in 2017"),

subtitle = paste("Incoming and outgoing passengers in millions,",

"with forecast data in blue."),

caption = paste("A. Jacobs :: unconj.ca\n",

"Data: Toronto Open Data (2016)\n",

"You may redistribute this graphic under",

"the terms of the CC-by-SA license."),

x = NULL, y = NULL)

## Scale for 'x' is already present. Adding another scale for 'x', which

## will replace the existing scale.

-

The author of the forecast package has recently revealed that future versions of the package will provide support for computing cross validation-like residuals. I may discuss incorporating this function in a future post. ↩︎